Learn how to optimise your equity, minimise your tax and maximise your wealth.

Simply fill out a few details below to get your copy:

Learn how to optimise your equity, minimise your tax and maximise your wealth.

Simply fill out a few details below to get your copy:

Want to help boost your retirement savings while potentially saving on tax? Here are five smart super strategies to consider before the end of the financial year.

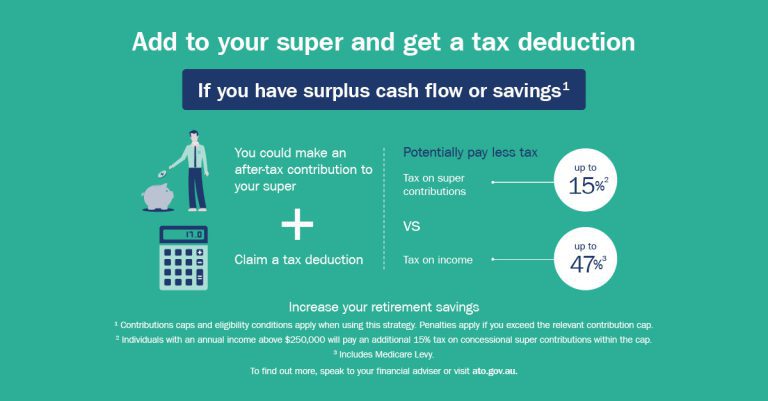

If you contribute some of your after-tax income or savings into super, you may be eligible to claim a tax deduction. This means you’ll reduce your taxable income for this financial year – and potentially pay less tax. And at the same time, you’ll be boosting your super balance.

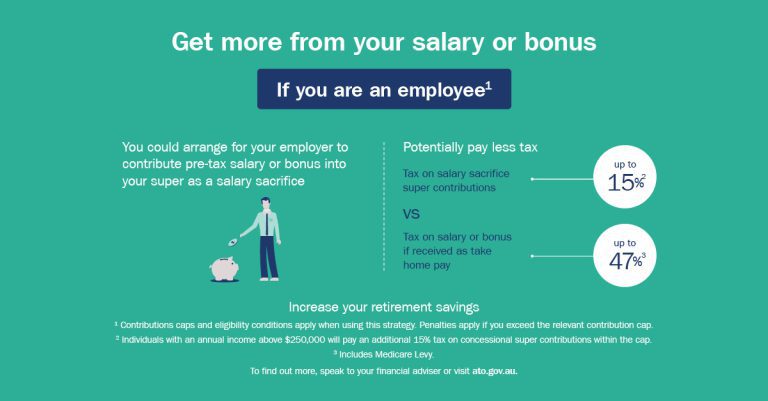

If you’re an employee, you may be able to arrange for your employer to direct some of your pre-tax salary or a bonus into your super as a “salary sacrifice” contribution.

Again, you’ll potentially pay less tax on this money than if you received it as take-home pay – generally 15% for those earning under $250,000 pa, compared with up to 47% (including Medicare Levy).

Another way to invest more in your super is with some of your after-tax income or savings, by making a personal non-concessional contribution.

Although these contributions don’t reduce your taxable income for the year, you can still benefit from the low tax rate of up to 15% that’s paid in super on investment earnings. This tax rate may be lower than what you’d pay if you held the money in other investments outside super.

If you earn less than $56,113 in the 2021/22 financial year, and at least 10% is from your job or a business, you may want to consider making an after- tax super contribution. If you do, the Government may make a ‘co-contribution’ of up to $500 into your super account.

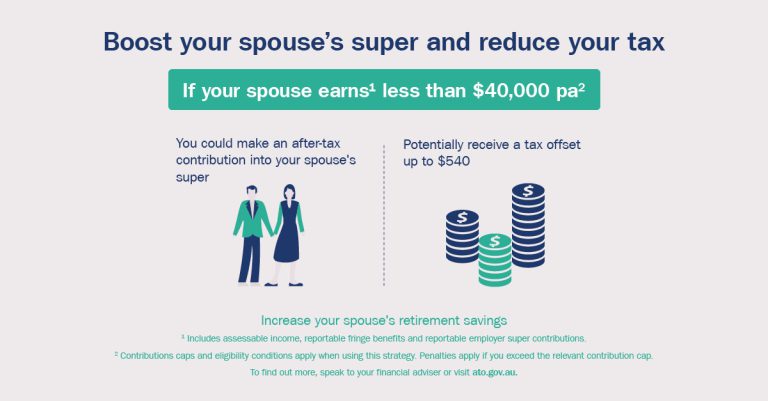

If your spouse is not working or earns a low income, you may want to consider making an after-tax contribution into their super account. This strategy could potentially benefit you both: your spouse’s super account gets a boost, and you may qualify for a tax offset of up to $540.

If you’re not sure about whether it is a good idea to put extra into superannuation or how to best maximise your superannuation for your retirement, click the image below to arrange a free consultation.

“The best way to measure your investing success is not by whether you’re beating the market but by whether you’ve put in place a financial plan and a behavioral discipline that are likely to get you where you want to go.”

~Benjamin Graham

In the world of personal finance, the term “financial thermostat” may sound peculiar at first. However, it serves as a powerful metaphor for understanding how individuals manage their money and financial goals. Just as a thermostat regulates temperature, a financial thermostat determines the financial mindset and behaviors that influence spending, saving, and investing. Understanding your financial thermostat is crucial for achieving long-term financial success and stability.

In the world of personal finance, the term “financial thermostat” may sound peculiar at first. However, it serves as a powerful metaphor for understanding how individuals manage their money and financial goals. Just as a thermostat regulates temperature, a financial thermostat determines the financial mindset and behaviors that influence spending, saving, and investing. Understanding your financial thermostat is crucial for achieving long-term financial success and stability.

Superannuation is one of the best tax-structures to fund your retirement, with currently no tax on capital gains or income once you transfer your accumulation account to an account-based pension.

You may wonder then, why is my superannuation split between taxable and tax-free? And how may this potentially impact my children?

In today’s rapidly evolving digital landscape, tech employees in Australia need to approach financial planning with a strategic mindset. Balancing equity compensation, performance bonuses, and retirement savings can be daunting, yet vital for long-term financial health. This article will explore essential strategic financial advice for tech employees and various tax planning and strategies specifically tailored […]

As a small business owner in Australia, planning for retirement is crucial for securing your financial future. One strategy available is an account-based pension, allowing you to draw a regular income from your superannuation while keeping the remaining balance invested. By implementing tailored retirement strategies now, you can work toward financial freedom and ensure a […]

Superannuation is a crucial aspect of retirement planning in Australia, especially for those in their 40s and 50s. As you approach retirement, understanding how to manage and maximise your superannuation is essential. This guide covers the basics, strategies, and common pitfalls to help you make the most of your super. Understanding Superannuation Basics Superannuation, or […]

Complete the form and we will schedule a chat at the most convenient time for you.

Learn how to optimise your equity, minimise your tax and maximise your wealth.

Simply fill out a few details below to get your copy: