100% free 23-page report details how to create an income for life, strategies to reduce tax and retire early!

Simply click the button below to get the free report

100% free 23-page report details how to create an income for life, strategies to reduce tax and retire early!

Simply click the button below to get the free report

It’s tax season! Let’s kick it off with some savvy strategies to boost your finances and set the stage for a brighter retirement.

Beware the pitfall: numerous high earners fall short of their retirement goals by underestimating their yearly super contributions.

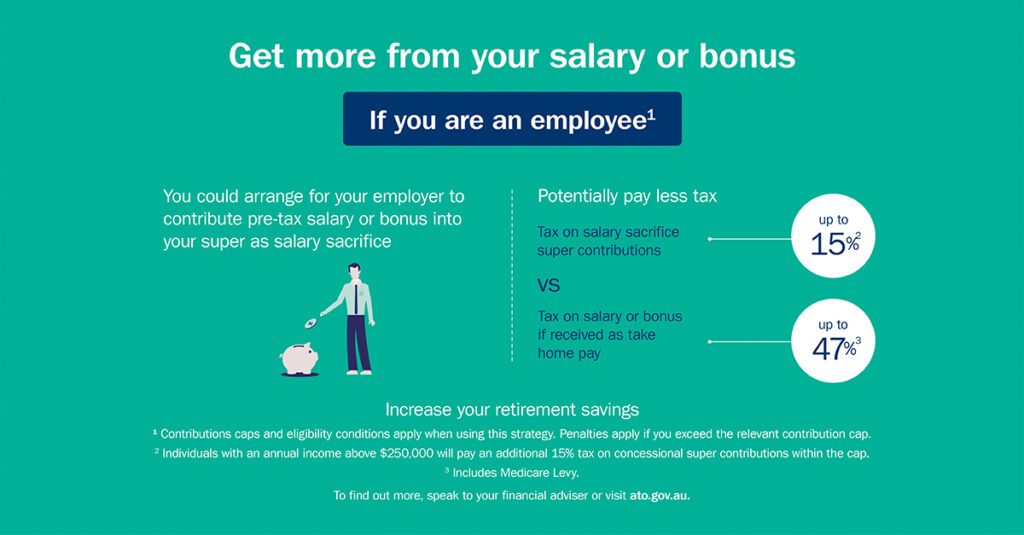

1. Salary sacrifice

Is an agreement between you and your employer to pay some of your pre-tax salary into super. This is often very tax effective. The amount you contribute to super is taxed at up to 15% (and up to 30% if your income is over $250,000 p.a.) rather than your marginal tax rate, which might be up to 47%. Salary sacrificed amounts to super are considered concessional contributions.

Depending on your circumstances, this strategy could result in a tax saving of up to 32% on the growth of your investments and enable you to increase your super.

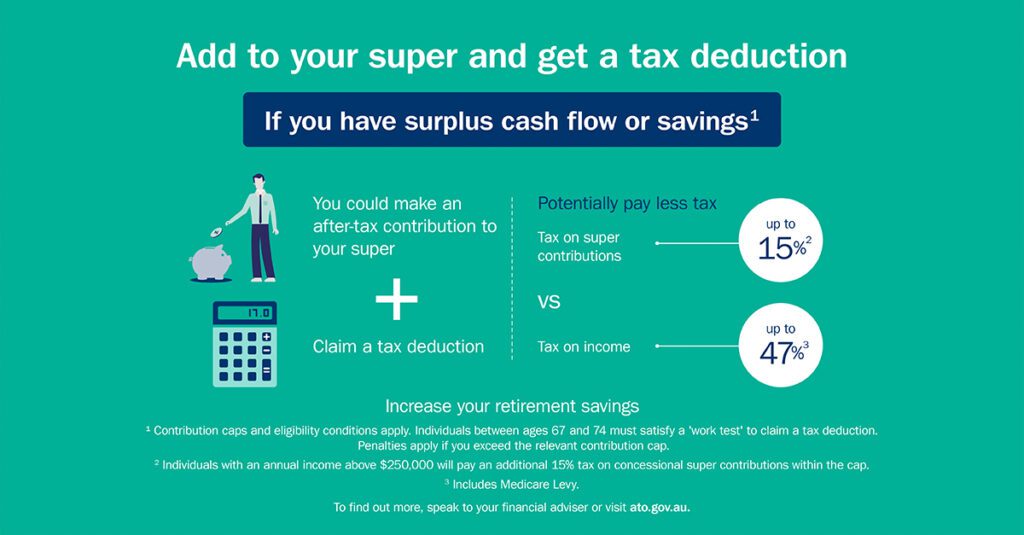

2. Personal deductible contributions

You can usually make your own personal contributions and claim a tax deduction for them to achieve the same tax outcome as salary sacrifice. This is a concessional contribution.

You can make a personal super contribution before 30 June and claim a tax deduction if you:

▪ want to tax-effectively top up employer super and salary sacrifice contributions

▪ terminate employment and receive taxable employment termination payments, or lump sum unused leave entitlements

▪ receive bonuses, or

▪ have taxable investment income and taxable capital gains from the sale of CGT assets.

To be eligible to claim the super contribution as a tax deduction, you need to submit a valid ‘Notice of Intent’ form to your super fund within required time frames. You will also need to receive an acknowledgement from the super fund before you complete your tax return, start a pension, withdraw or rollover money from the fund to which you made your personal contribution.

Did you know the annual concessional contribution cap is increasing to $30,000 in FY 2024/25 as well as the Superannuation Guarantee contributions rate which is going from 11% to 11.5% of your salary.

3. Non-concessional contributions (NCCs)

NCC’s are personal contributions to super made from post-tax income or available capital, exempt from contributions tax.

There’s an annual cap for NCCs, currently set at $110,000 for 2023/24, four times the annual concessional contribution (CC) cap.

Individuals under 75 as of 1 July in a financial year can potentially bring forward up to two years of NCCs, allowing for a larger upfront contribution.

Starting July 1 this year, the annual NCC cap increases to $120,000, with a new three-year bring-forward option rising to $360,000.

Timing is crucial when activating the new NCC bring-forward rule. Many clients have already contributed $110,000 this year and plan to trigger the three-year bring forward next year, potentially adding $360,000 more.

This could mean each parent can inject $470,000 into their super within the next two months!

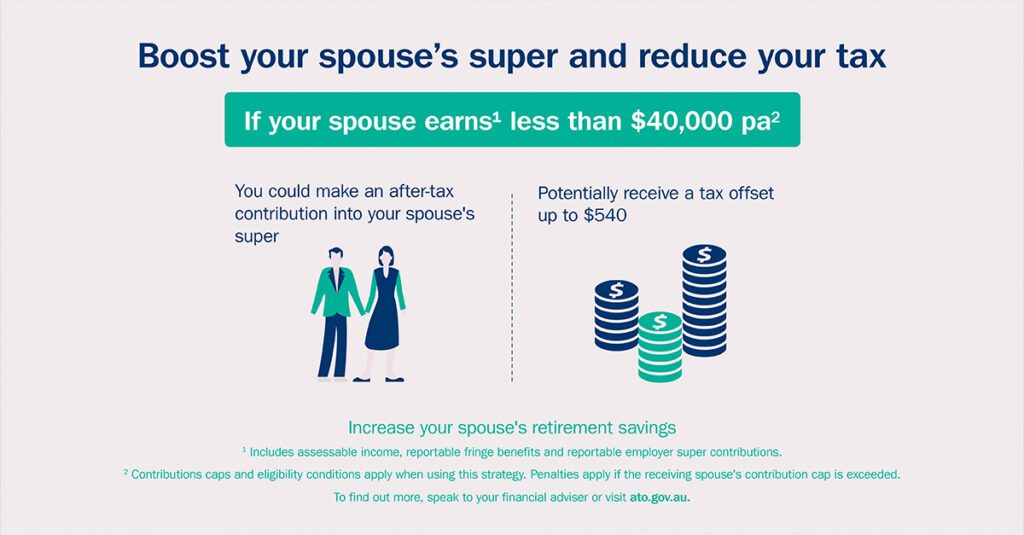

4. Spouse contributions

By contributing to your spouse’s superannuation, you can enhance their retirement savings.

Eligible individuals can receive a tax offset of up to $540 by making super contributions of up to $3,000 into their spouse’s account if their spouse earns $37,000 or less annually in 2023/24.

This contribution falls under the non-concessional category.

5. Contribution splitting

Contribution splitting offers the option to redirect a portion of your superannuation into your partner’s account.

A client may choose to divide qualifying concessional contributions from the previous financial year into their spouse’s super account in the subsequent year.

This strategy can assist eligible clients in harmonising their super balances as a couple.

If there is a plan to split personal deductible contributions, the Notice of Intent must be submitted and confirmed by the fund prior to initiating the contribution splitting process.

6. Catch-up contributions

If your concessional contributions (CCs) in a given financial year fall below the annual cap, you can carry forward these unused amounts for up to five years. This allows you to potentially contribute more in a future year if you meet eligibility criteria.

The flexibility to make larger contributions when suitable can be beneficial, especially if you experience irregular income or have a significant capital gains tax liability.

To utilise your carried forward CCs via catch-up contributions, your total superannuation balance must be under $500,000 as of the previous 30th of June, and you must have unused CC cap amounts accumulated from the past five financial years.

To learn more about this strategy check out my recent blog https://www.deltafinancialgroup.com.au/catch-up-contributions/

7. Co-contributions

Your spouse has the opportunity to enhance their super account by making an after-tax contribution.

This action could lead to a government contribution of up to $500, known as a ‘co-contribution.’

For your spouse to qualify for the maximum co-contribution in the financial year 2023/24, they must contribute $1,000 or more to their super while earning $43,445 or less.

8. Double deductions (SMSFs)

An SMSF member can strategically boost their tax benefits by making a personal contribution in one financial year, claiming the deduction, and aligning it with the following year’s concessional contribution cap.

This tactic maximises the deductible amount in any given fiscal year.

For personal contributions to an SMSF, timely allocation to the member’s account is crucial, typically within 28 days after the end of the following month post-contribution.

For instance, a contribution made on 1 June must be allocated by 28 July to enable the member to claim a tax deduction for their super contribution in the year of contribution.

9. Manage Div 293 tax

Division 293 tax is an additional levy on super contributions, decreasing tax benefits for individuals with combined income and concessional contributions exceeding $250,000 for Division 293.

The first-time liability for Div 293 tax may arise in the upcoming financial year due to factors like redundancy, termination payments, or significant capital gains in 2023/24.

Eligibility for catch-up contributions could raise a person’s CC cap, potentially leading to higher Division 293 tax obligations. Nonetheless, individuals subject to Div 293 tax will pay a lower overall tax on their CCs compared to the marginal tax rate on taxable income.

Payment of Division 293 Tax can be made using personal funds or by opting to withdraw it from any existing superannuation accounts.

10. Buy insurance inside super

Purchasing insurance within your superannuation fund offers tax benefits. Life and Total Permanent Disability (TPD) insurance premiums are tax-deductible when owned by your super fund. However, the same policy isn’t tax-deductible when held in your personal name.

Moreover, income protection payments can be made from your super fund to avoid impacting your personal cash flow.

11. Pre-pay deductible expenses

To accelerate the tax deduction and lower taxable income in 2023/24, consider pre-paying specific expenses.

If you anticipate a decrease in your marginal tax rate starting July 1, 2024, due to the Stage 3 tax cuts, advancing the deduction to 2023/24 could yield additional advantages.

Examples of deductible expenses eligible for pre-payment include:

– Premiums for income protection policies held outside superannuation

– Interest on fixed-rate investment loans

– Costs related to a rental property

– Work-related subscriptions

12. Manage CGT on asset sales

There are a range of strategies that could be used to manage capital gains tax (CGT) that may be payable when disposing of assets. These include:

▪ deferring the sale until the asset has been held for 12 months to benefit from the 50% CGT discount

▪ deferring the sale to another financial year if taxable income will be lower

▪ spreading the sale over several years to smooth out the impact on taxable income in any given year

▪ selling assets that trigger a capital loss to offset gains made on other assets in the same financial year

▪ offsetting any realised capital losses against gains from assets not eligible for the 50% discount, and

▪ making a personal deductible super contribution (perhaps by also utilising the catch-up rules) to offset some or all of a taxable capital gain from the sale of an asset in the same financial year.

#1: Ready to grow your personal wealth? Let’s chat >>Click here to book your 1:1 free strategy call with me

#2: Follow me on LinkedIn and Facebook for more personal finance tips

#3: Read what success looks like with 4.8 Stars from 135 Customer Reviews across Google Reviews & LinkedIn

#4: Read my latest article ebook >>> The Ultimate Retirement Guide to Create An Income For Life

“The best way to measure your investing success is not by whether you’re beating the market but by whether you’ve put in place a financial plan and a behavioral discipline that are likely to get you where you want to go.”

~Benjamin Graham

In the world of personal finance, the term “financial thermostat” may sound peculiar at first. However, it serves as a powerful metaphor for understanding how individuals manage their money and financial goals. Just as a thermostat regulates temperature, a financial thermostat determines the financial mindset and behaviors that influence spending, saving, and investing. Understanding your financial thermostat is crucial for achieving long-term financial success and stability.

In the world of personal finance, the term “financial thermostat” may sound peculiar at first. However, it serves as a powerful metaphor for understanding how individuals manage their money and financial goals. Just as a thermostat regulates temperature, a financial thermostat determines the financial mindset and behaviors that influence spending, saving, and investing. Understanding your financial thermostat is crucial for achieving long-term financial success and stability.

Superannuation is one of the best tax-structures to fund your retirement, with currently no tax on capital gains or income once you transfer your accumulation account to an account-based pension.

You may wonder then, why is my superannuation split between taxable and tax-free? And how may this potentially impact my children?

In today’s rapidly evolving digital landscape, tech employees in Australia need to approach financial planning with a strategic mindset. Balancing equity compensation, performance bonuses, and retirement savings can be daunting, yet vital for long-term financial health. This article will explore essential strategic financial advice for tech employees and various tax planning and strategies specifically tailored […]

As a small business owner in Australia, planning for retirement is crucial for securing your financial future. One strategy available is an account-based pension, allowing you to draw a regular income from your superannuation while keeping the remaining balance invested. By implementing tailored retirement strategies now, you can work toward financial freedom and ensure a […]

Superannuation is a crucial aspect of retirement planning in Australia, especially for those in their 40s and 50s. As you approach retirement, understanding how to manage and maximise your superannuation is essential. This guide covers the basics, strategies, and common pitfalls to help you make the most of your super. Understanding Superannuation Basics Superannuation, or […]

Complete the form and we will schedule a chat at the most convenient time for you.

100% free 23-page report details how to create an income for life, strategies to reduce tax and retire early!

Simply click the button below to get the free report