100% free 23-page report details how to create an income for life, strategies to reduce tax and retire early!

Simply click the button below to get the free report

100% free 23-page report details how to create an income for life, strategies to reduce tax and retire early!

Simply click the button below to get the free report

Superannuation is a crucial aspect of financial planning, especially when it comes to retirement. It refers to the funds accumulated throughout a person’s working life to provide income during their retirement years. This article aims to provide a comprehensive guide to understanding superannuation, different types of superannuation funds, key factors to consider, and strategies for maximising your superannuation.

Superannuation plays a fundamental role in ensuring financial security during retirement. But what exactly is superannuation?

Superannuation, commonly referred to as super, is a long-term savings vehicle that helps individuals accumulate wealth to support their lifestyle after they retire from the workforce.

Most Australians are eligible to contribute to super, and it is compulsory for employers to make regular superannuation contributions on behalf of their employees.

Superannuation is not just a simple savings account; it is a complex system designed to provide individuals with tax benefits and investment growth opportunities to secure their financial future.

Contributions to super are made regularly, either through employer contributions or personal contributions made by individuals. These funds are then invested by superannuation funds to generate returns over time.

Superannuation funds are regulated by the Australian Prudential Regulation Authority (APRA) to ensure the security and integrity of retirement savings. APRA sets strict guidelines and monitors the performance of superannuation funds to protect the interests of fund members.

When it comes to retirement planning, superannuation plays a crucial role. It forms the backbone of retirement planning, providing individuals with a reliable income stream to support their lifestyle when they are no longer working full-time.

Relying solely on government-funded pensions may not be sufficient to meet your financial needs during retirement, which is why superannuation is crucial. By planning and contributing to your superannuation fund throughout your working years, you can build a substantial nest egg that will support you during your post-employment years.

Superannuation funds come in different forms, catering to different preferences and requirements. Let’s explore the most common types:

Industry super funds are run by employer associations and unions and are widely available to employees across industries. These funds generally offer competitive fees and a range of investment options.

One of the key benefits of industry super funds is their not-for-profit status, which means profits are reinvested into the fund for the benefit of members.

Industry super funds often have a strong focus on specific industries, such as construction, healthcare, or education. This specialization allows them to tailor their services and investment options to the needs of their members. For example, an industry super fund for healthcare workers may offer additional benefits like discounted health insurance or access to professional development programs.

In addition to competitive fees, industry super funds often provide comprehensive insurance coverage for members. This can include life insurance, total and permanent disability insurance, and income protection insurance. Having insurance through your superannuation fund can provide peace of mind and financial protection for you and your loved ones.

Retail super funds are managed by financial institutions such as banks or insurance companies. They are typically open to anyone and offer a variety of investment options.

Some retail funds may have higher fees compared to industry super funds, so it’s essential to consider the costs and benefits before making a decision.

One advantage of retail super funds is the ability to access a wide range of investment options. These options can include shares, property, fixed interest investments, and even alternative assets like infrastructure or commodities. This flexibility allows investors to create a diversified portfolio that aligns with their risk tolerance and investment goals.

Furthermore, retail super funds often provide additional services and benefits to their members. These can include financial planning advice, educational resources, and access to discounted products or services from affiliated companies. For example, a retail super fund associated with a bank may offer preferential interest rates on home loans or credit cards for its members.

Self-Managed Super Funds (SMSFs) provide individuals with greater control over their superannuation investments. With an SMSF, you become a trustee responsible for managing the fund’s investments and compliance with regulatory requirements.

While SMSFs offer flexibility and control, they also require a significant amount of time, effort, and financial knowledge to manage effectively. Therefore, SMSFs are generally suitable for those with substantial superannuation balances or complex investment strategies.

One of the main advantages of an SMSF is the ability to invest in a wide range of assets. This can include direct property, unlisted assets, and even collectibles like artwork or vintage cars. The flexibility to invest in these alternative assets can provide diversification and potentially higher returns for SMSF members.

However, managing an SMSF involves various responsibilities and obligations. These include keeping accurate records, preparing financial statements and tax returns, and ensuring compliance with superannuation laws and regulations. It is essential to seek professional advice from accountants, auditors, and financial advisors to ensure you meet all legal requirements and make informed investment decisions.

Additionally, SMSFs must have an investment strategy that considers the members’ risk profile, investment objectives, and cash flow requirements. This strategy should be regularly reviewed and updated to reflect any changes in personal circumstances or market conditions.

In conclusion, the choice of superannuation fund depends on individual preferences, financial goals, and investment knowledge. Whether you opt for an industry super fund, retail super fund, or self-managed super fund, it is crucial to consider factors such as fees, investment options, insurance coverage, and the level of control and responsibility you are comfortable with. Seeking professional advice can help you make an informed decision and maximise the benefits of your superannuation savings.

How much do I need to retire? Watch my 1 minute video

When it comes to superannuation, several essential factors can significantly impact your retirement savings. Let’s explore each in detail:

Superannuation funds offer a range of investment options, such as shares, property, cash, and fixed interest. It’s crucial to consider your risk tolerance, investment goals, and time horizon when selecting the most suitable investments for your superannuation portfolio.

For example, if you have a higher risk tolerance and a longer time horizon until retirement, you may consider investing a larger portion of your superannuation in growth assets such as shares or property. On the other hand, if you have a lower risk tolerance or a shorter time horizon, you may opt for more conservative investments like cash or fixed interest.

Seeking professional advice or consulting a Sydney financial planner can help you make informed investment decisions aligned with your retirement goals. They can provide personalised recommendations based on your individual circumstances and help you navigate the complexities of the investment market.

Superannuation funds charge various fees, such as administration fees, investment management fees, and insurance premiums. These fees can significantly impact your retirement savings over the long term.

It’s important to understand the fee structure of your superannuation fund and compare the costs across different funds. While fees are necessary to cover the expenses of managing your superannuation, it’s essential to ensure that you are not paying excessive fees that eat into your returns.

Always aim for a fund with competitive fees without compromising on investment options or services. Some funds may offer lower fees but may lack the investment options or customer service that you desire. Therefore, it’s crucial to strike a balance between fees and the value provided by the fund.

Superannuation funds often offer insurance coverage, including life insurance, total and permanent disability (TPD) insurance, and income protection insurance. It’s important to review the insurance coverage provided by your fund to ensure it aligns with your needs.

Consider factors such as the level of coverage, premium costs, waiting periods, and any exclusions or limitations associated with the insurance policies provided by your superannuation fund. It’s crucial to understand the terms and conditions of the insurance coverage to make an informed decision.

For example, if you have dependents or significant financial obligations, having adequate life insurance coverage can provide financial security to your loved ones in the event of your untimely demise. Similarly, income protection insurance can provide a safety net if you are unable to work due to illness or injury.

Reviewing your insurance coverage regularly is also important as your circumstances may change over time. For instance, if you have recently gotten married, had children, or taken on additional financial responsibilities, you may need to adjust your insurance coverage accordingly.

Contribution strategies can be the turbo-boosters of your super, propelling you closer to your desired retirement lifestyle.

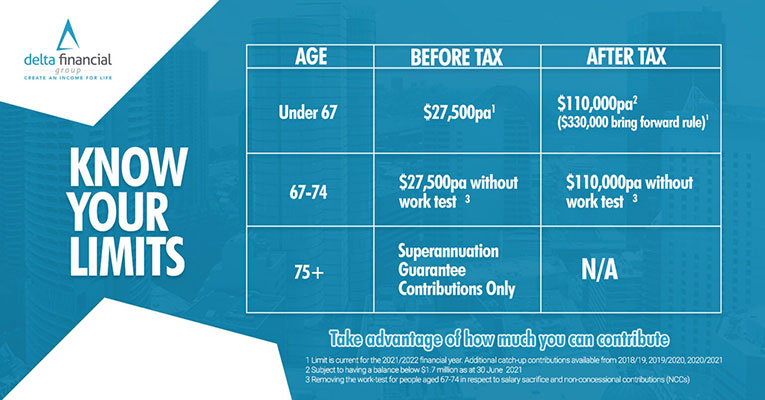

If you’re able to contribute more than your required superannuation contribution, you should consider making non-concessional contributions of $110,000 each year, which are after-tax contributions that do not attract additional contributions tax.

A strategic move for many, salary sacrificing can be a tax-effective method to boost your super. This is where you and your employer agree to reduce your salary in exchange for additional super contributions.

Catch up contributions allow you to make additional concessional contributions to your superannuation if you have not reached your concessional contributions cap in the previous 5 years. Keep in mind that to use this feature, you must meet certain conditions, such as having a total super balance below $500,000 at the end of the previous financial year.

Utilising unused cap amounts can be extremely useful where you need to make a large one-off contribution to reduce capital gains tax arising from, say, the sale of an investment property.

The government might help you help yourself. If you earn less than $58,445 a year, you might be eligible for a government co-contribution, which matches a portion of your after-tax contributions.

The baby boomer generation typify the pinnacle of retirement planning, with unique strategies to match.

Making voluntary super contributions is a great way to boost your retirement savings and potentially reduce the amount of tax you pay. It can also provide a tax-effective way to transition to retirement.

The 3 year bring forward option allows individuals under the age of 65 to make up to three times the annual non-concessional contribution limit in a single financial year, so $330,000 for each person.

You may be eligible to make a downsizer contribution of up to $300,000 ($600,000 for a couple) if you sell a home that you or your spouse owned for at least 10 years and contribute the proceeds within 90 days of settlement. The minimum age to make a downsizer contribution is now 55, down from 60 (originally 65).

A downsizer contribution allows you to boost your super even if you’re otherwise ineligible to contribute due to age or TSB – meaning you can still contribute even if you’re aged 75 or more or have $1.9 million or more in super.

For couples with one spouse who has a higher super balance, it may be beneficial to split some of their contributions into the lower balance account, helping them both qualify for benefits and reduce taxes.

Being tax-savvy in retirement is all about ensuring your sources of income are structured to minimise your tax liability, leaving you with more to enjoy. Consider seeking professional advice to maximise your savings.

In conclusion, superannuation is a vital component of retirement planning. Understanding the basics of superannuation, exploring different types of superannuation funds, considering key factors, and implementing effective strategies can make a significant difference in maximising your retirement savings.

Contact our sydney financial advisors today at 02 9327 4338 for personalised superannuation advice that can transform your retirement dreams into a tangible, prosperous reality. Remember, the most potent wealth is knowledge—so educate yourself, seek guidance, and take charge of your financial future today.

“The best way to measure your investing success is not by whether you’re beating the market but by whether you’ve put in place a financial plan and a behavioral discipline that are likely to get you where you want to go.”

~Benjamin Graham

In the world of personal finance, the term “financial thermostat” may sound peculiar at first. However, it serves as a powerful metaphor for understanding how individuals manage their money and financial goals. Just as a thermostat regulates temperature, a financial thermostat determines the financial mindset and behaviors that influence spending, saving, and investing. Understanding your financial thermostat is crucial for achieving long-term financial success and stability.

In the world of personal finance, the term “financial thermostat” may sound peculiar at first. However, it serves as a powerful metaphor for understanding how individuals manage their money and financial goals. Just as a thermostat regulates temperature, a financial thermostat determines the financial mindset and behaviors that influence spending, saving, and investing. Understanding your financial thermostat is crucial for achieving long-term financial success and stability.

Superannuation is one of the best tax-structures to fund your retirement, with currently no tax on capital gains or income once you transfer your accumulation account to an account-based pension.

You may wonder then, why is my superannuation split between taxable and tax-free? And how may this potentially impact my children?

In today’s rapidly evolving digital landscape, tech employees in Australia need to approach financial planning with a strategic mindset. Balancing equity compensation, performance bonuses, and retirement savings can be daunting, yet vital for long-term financial health. This article will explore essential strategic financial advice for tech employees and various tax planning and strategies specifically tailored […]

As a small business owner in Australia, planning for retirement is crucial for securing your financial future. One strategy available is an account-based pension, allowing you to draw a regular income from your superannuation while keeping the remaining balance invested. By implementing tailored retirement strategies now, you can work toward financial freedom and ensure a […]

Superannuation is a crucial aspect of retirement planning in Australia, especially for those in their 40s and 50s. As you approach retirement, understanding how to manage and maximise your superannuation is essential. This guide covers the basics, strategies, and common pitfalls to help you make the most of your super. Understanding Superannuation Basics Superannuation, or […]

Complete the form and we will schedule a chat at the most convenient time for you.

100% free 23-page report details how to create an income for life, strategies to reduce tax and retire early!

Simply click the button below to get the free report